PT Trimegah Bangun Persada Tbk's management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

Management's newest company overview: current volumes and financials across all three routes, the project pipeline, and why certification gates market access. · Open the full document →

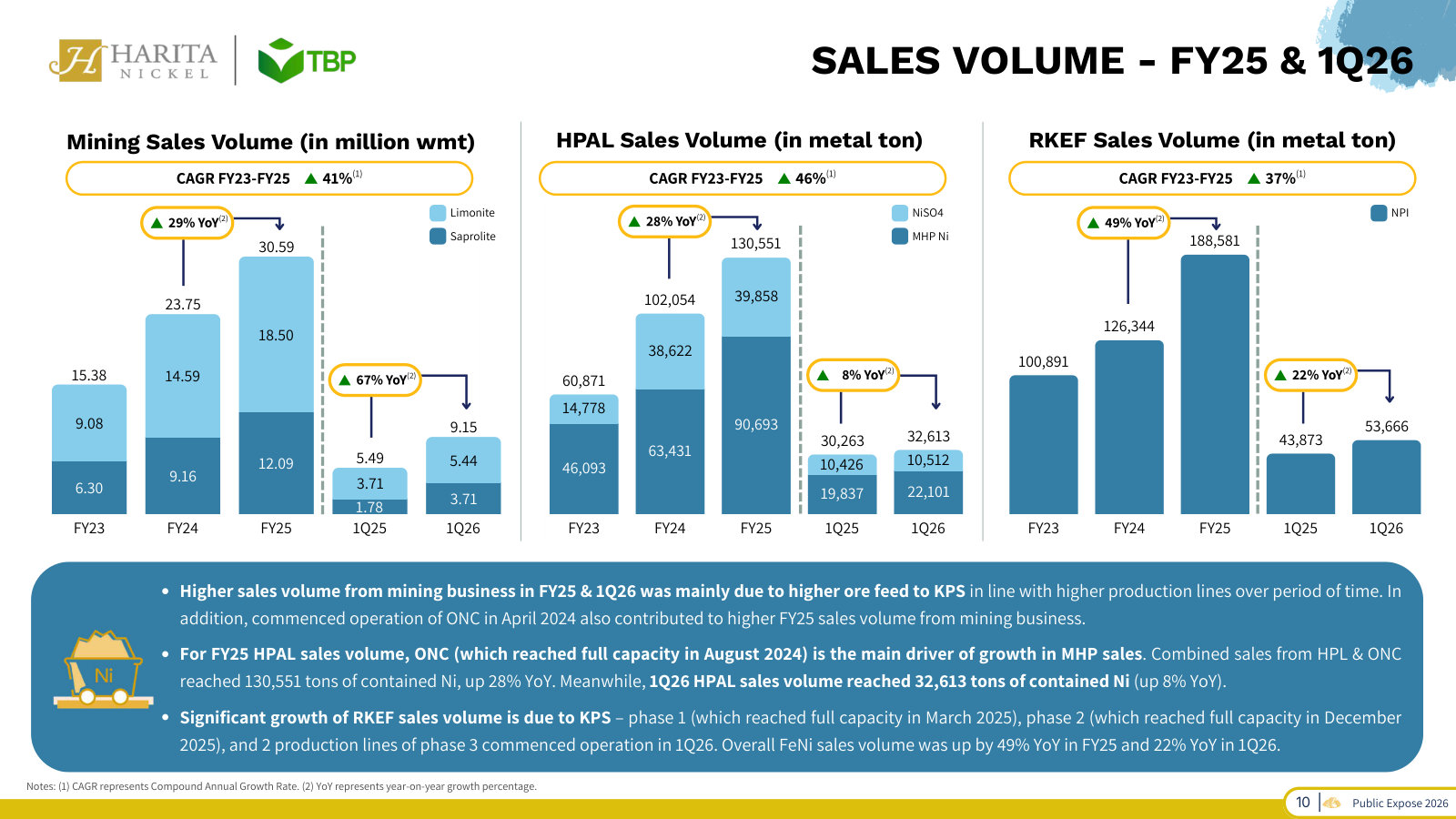

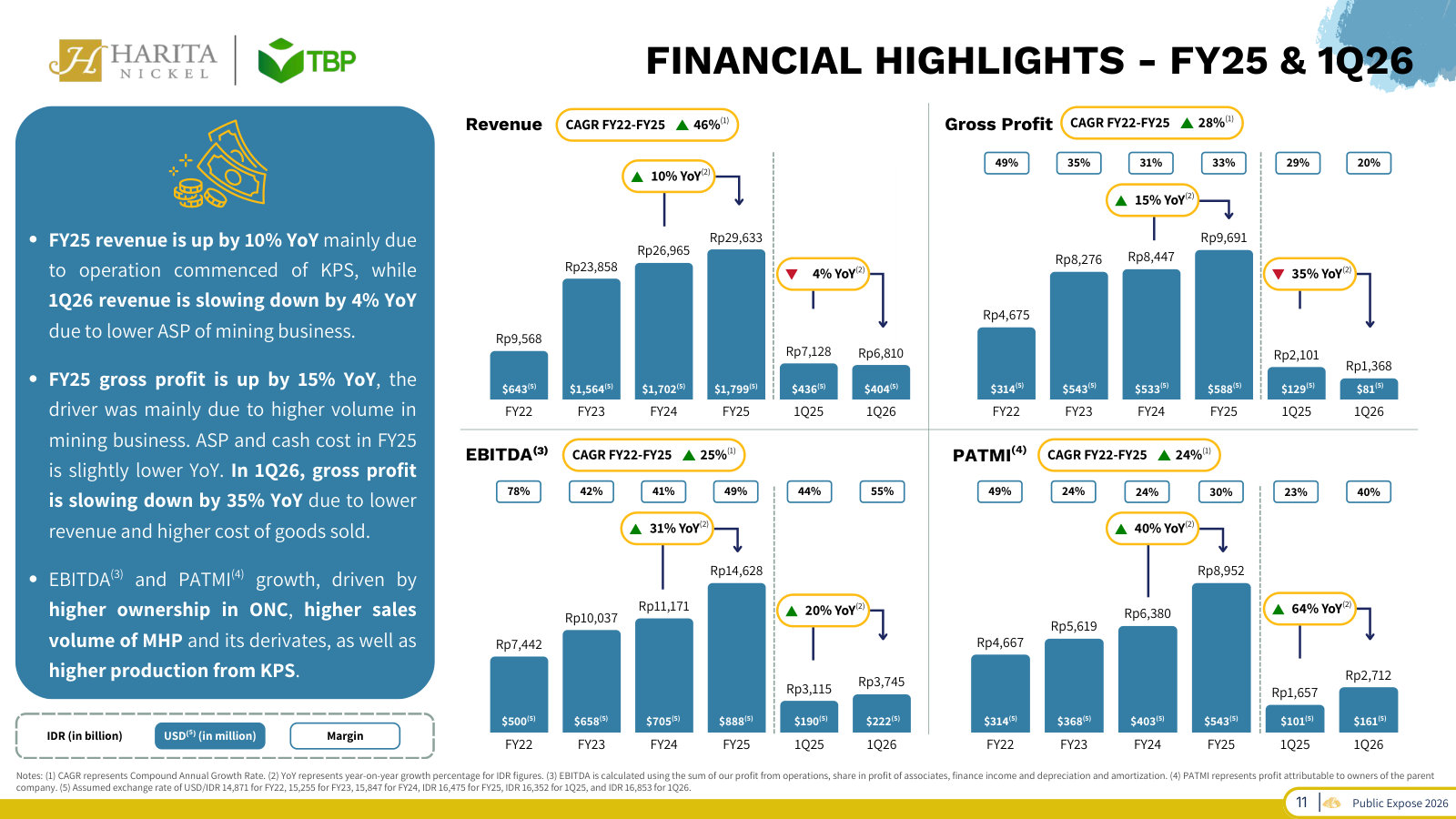

p. 6 — KPS, the third RKEF smelter (185kt Ni/yr of FeNi in 12 lines): phase 2 complete and producing, phase 3 at 94% — the near-term growth engine. · Open the full presentation →p. 7 — Quicklime plant (CKM): making its own quicklime from limestone to cut HPAL reagent cost — a small vertical-integration step, 98% built. · Open the full presentation →p. 8 — Iron-extraction pilot: pulling saleable iron out of HPAL tailings — an attempt to turn processing waste into a new product. · Open the full presentation →p. 10 — Sales volume FY23–1Q26 across the three routes: mining (limonite/saprolite), HPAL (MHP/nickel sulfate) and RKEF (FeNi), split by product. · Open the full presentation →p. 11 — Revenue, gross profit, EBITDA and PATMI with margins, FY22–1Q26 — profitability and the recent margin squeeze from softer nickel prices. · Open the full presentation →p. 13 — IRMA / RMAP certifications: responsible-sourcing audits that keep product eligible for EU and China battery supply chains — a market gate. · Open the full presentation →

The fullest walk-through of how the business is actually built — geography, the two processing routes, ports, capacity by product, and per-product economics — content later decks dropped. · Open the full document →

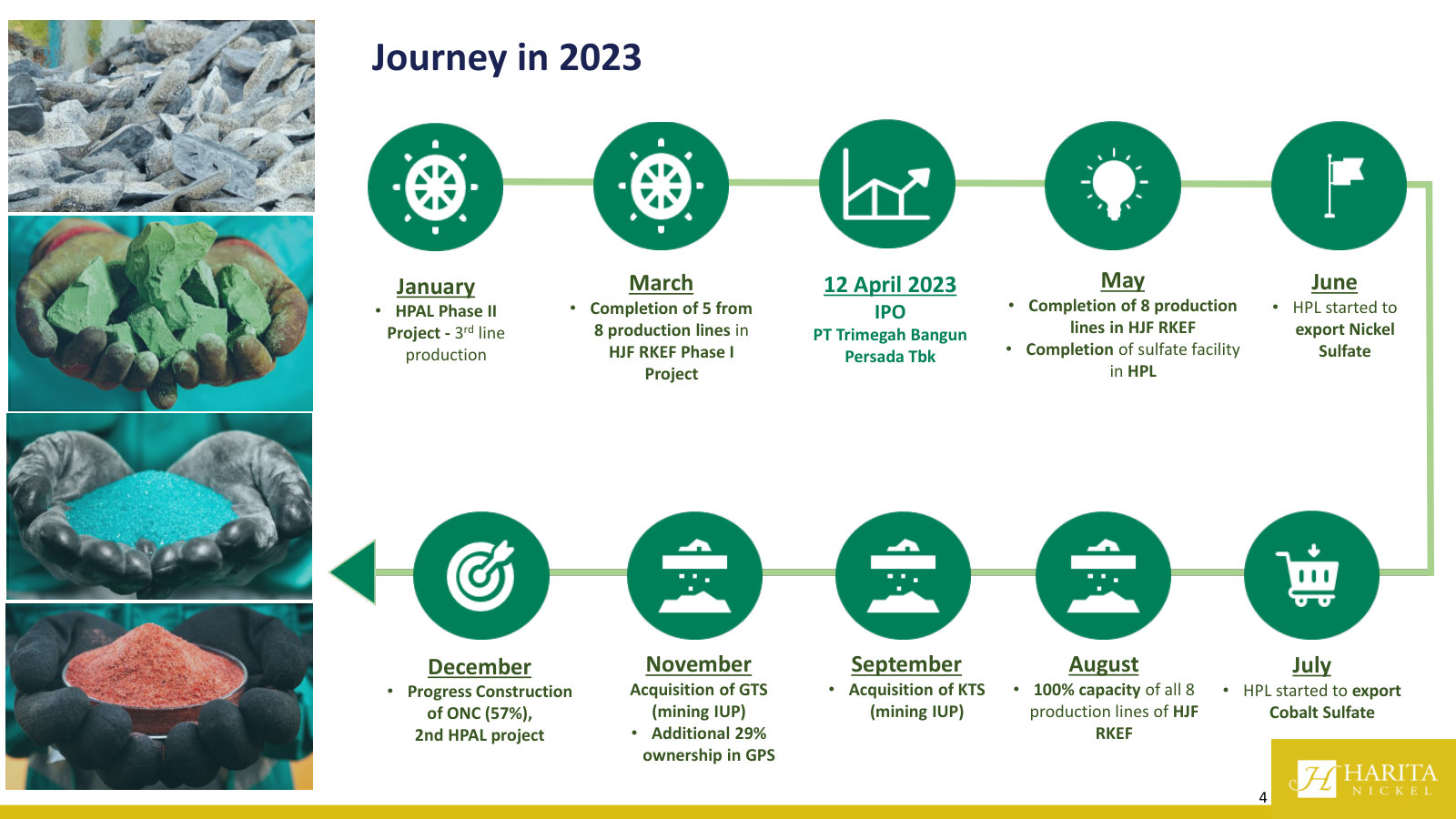

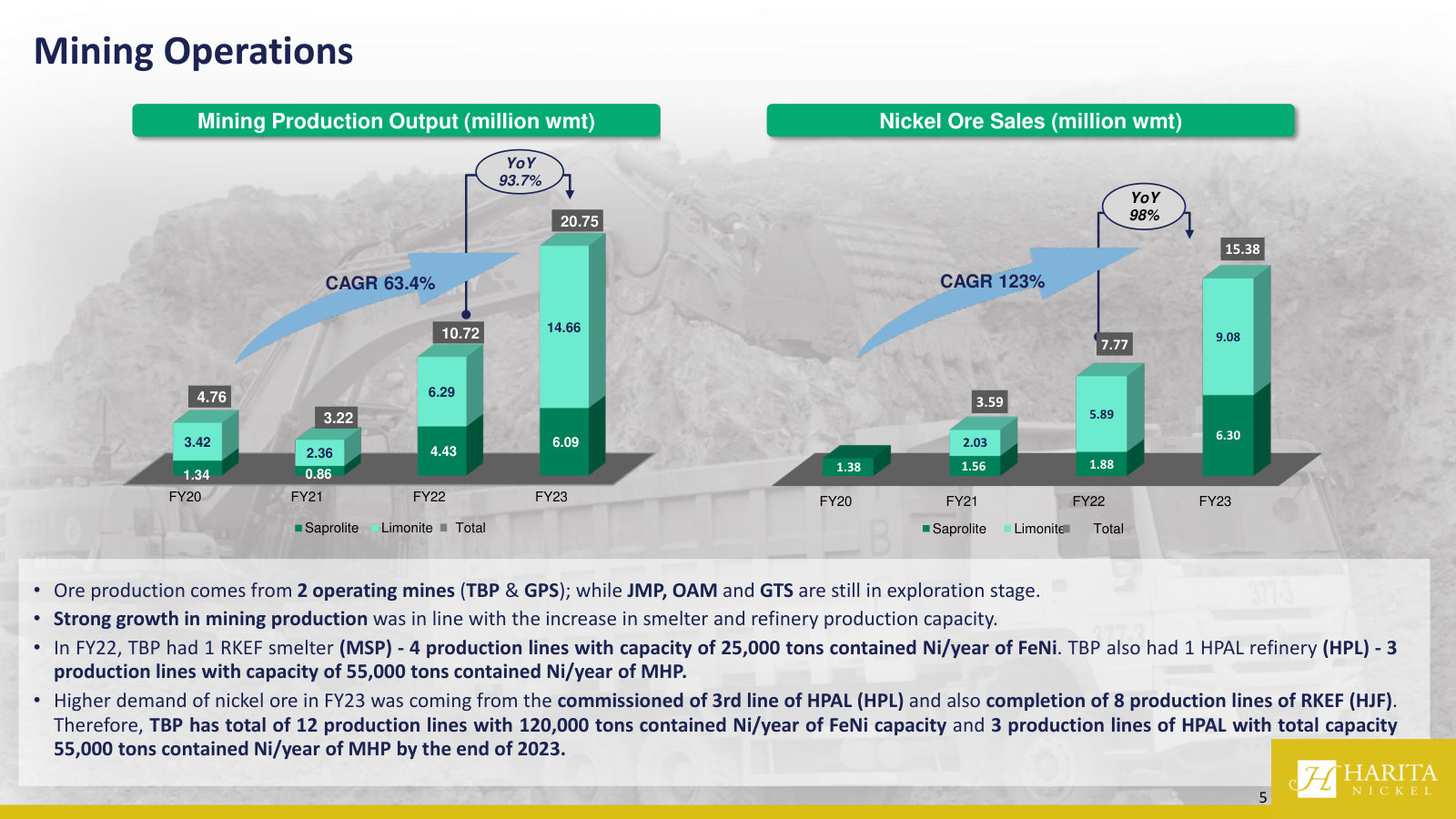

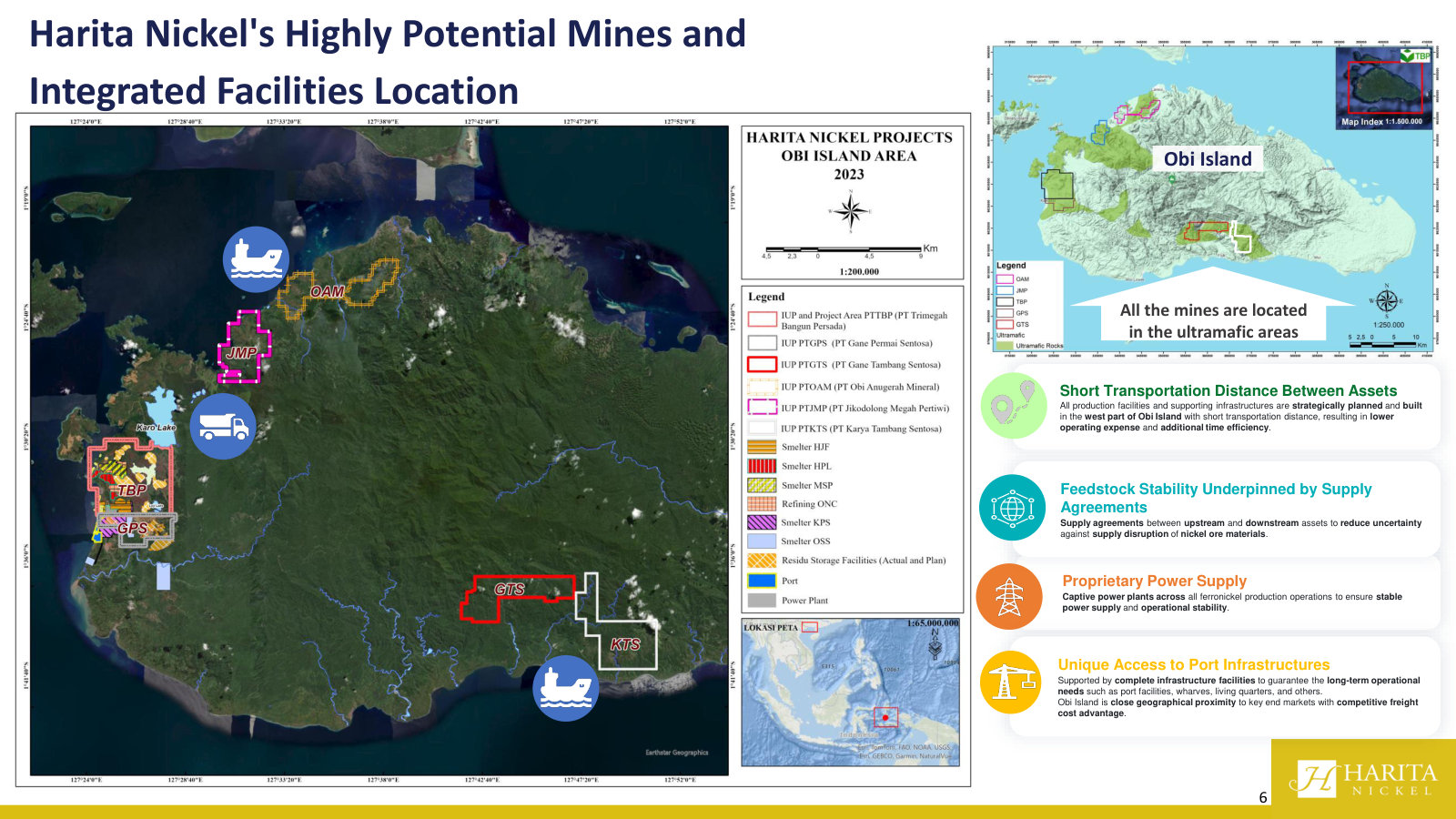

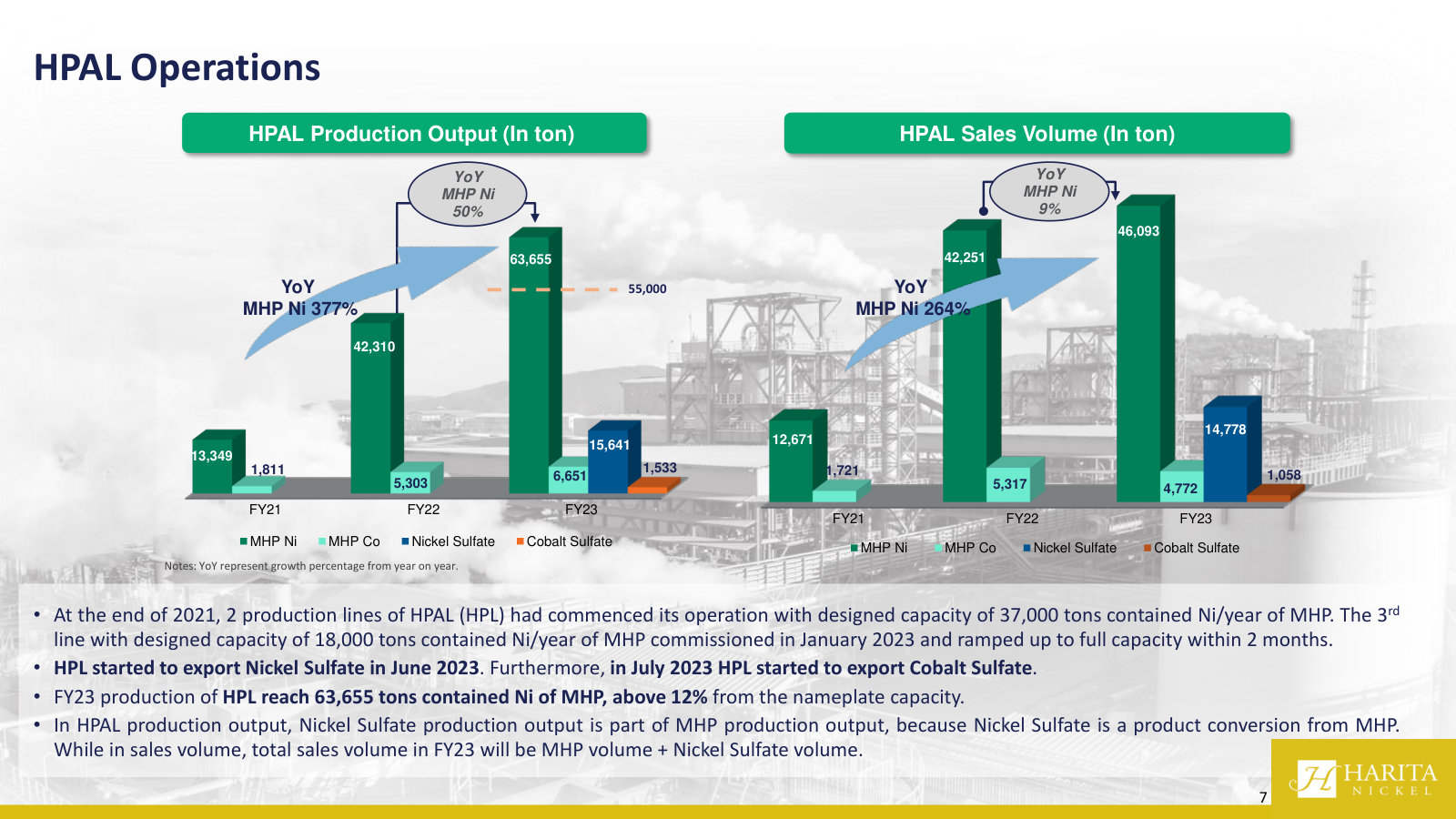

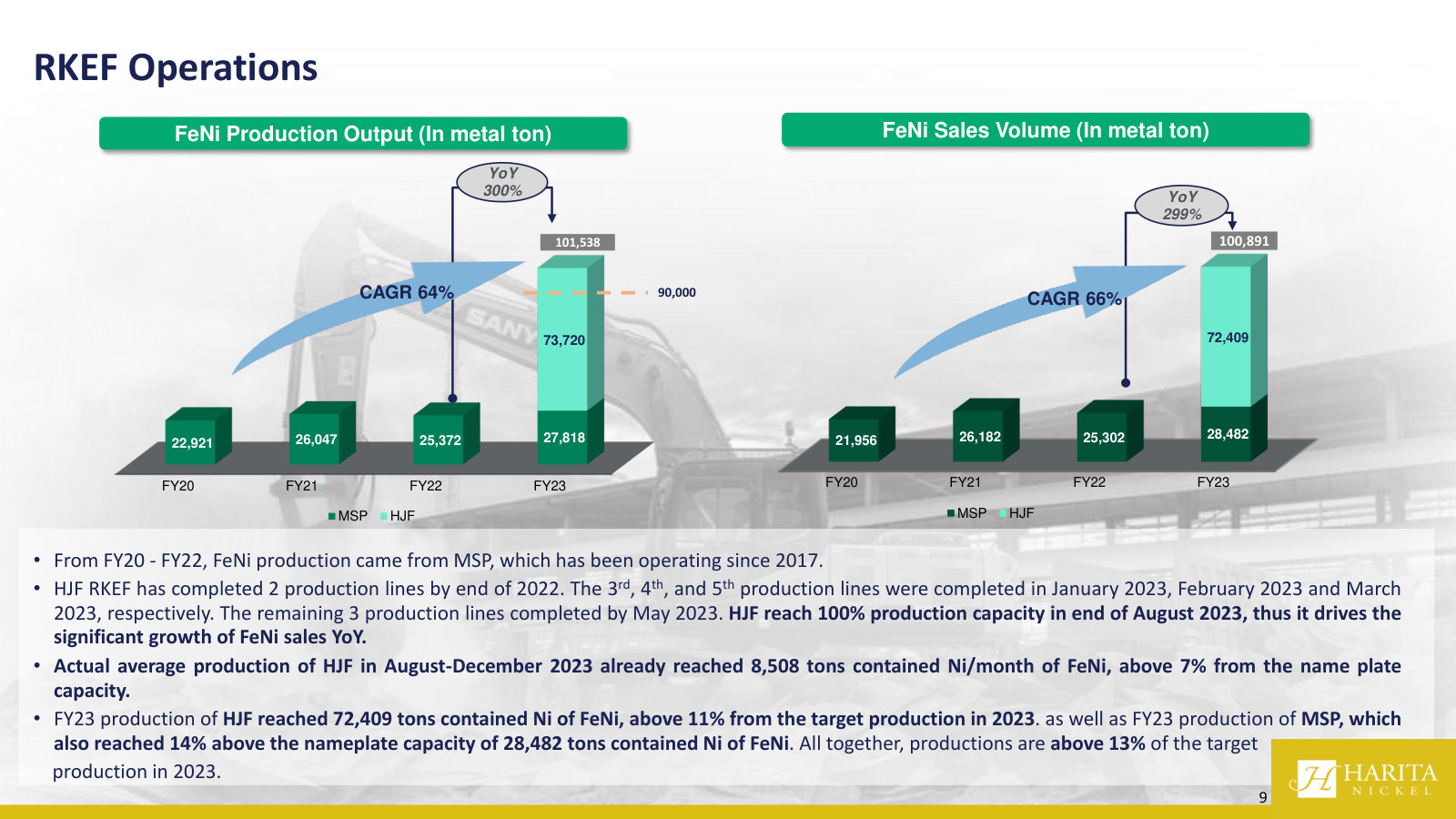

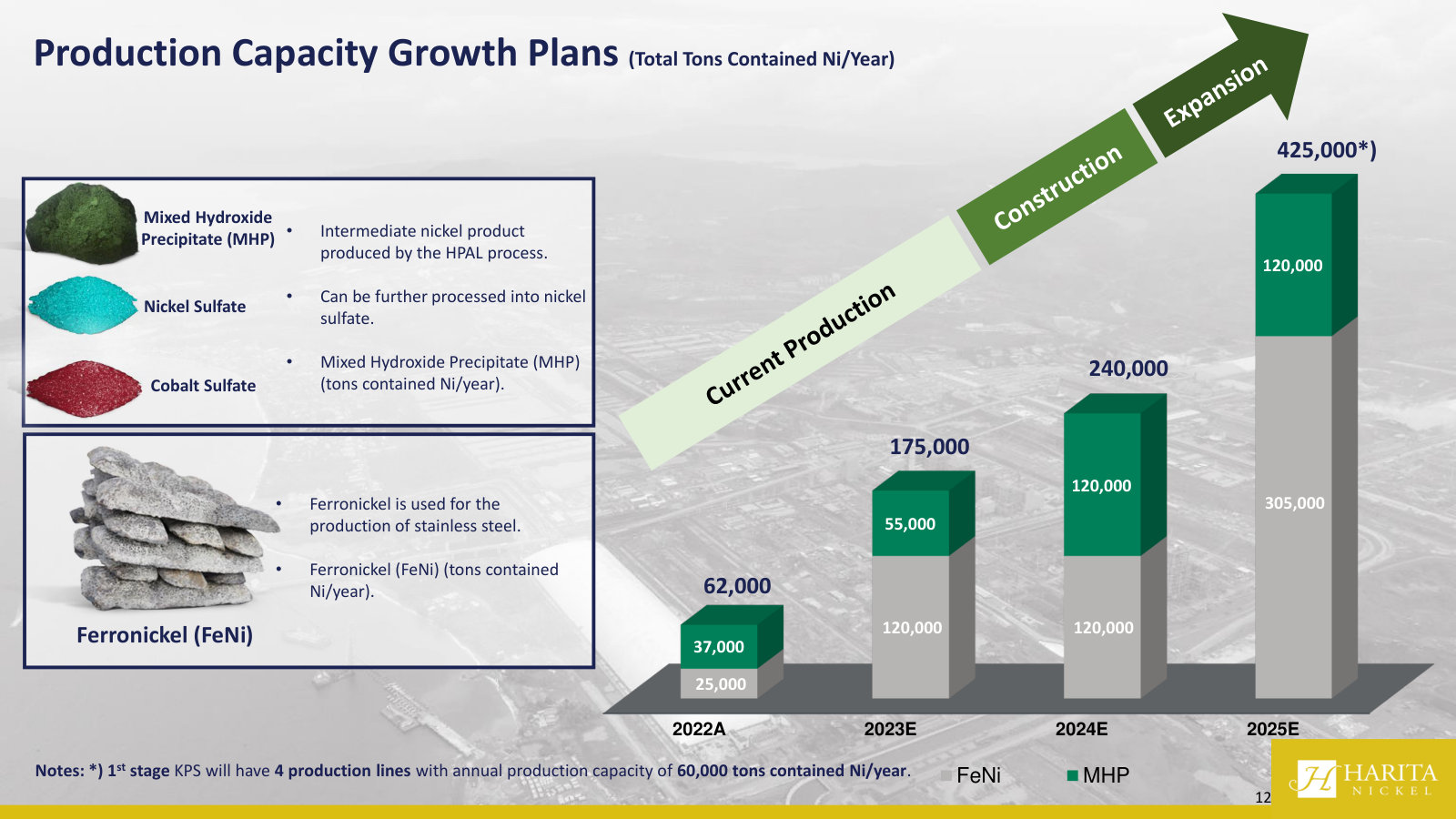

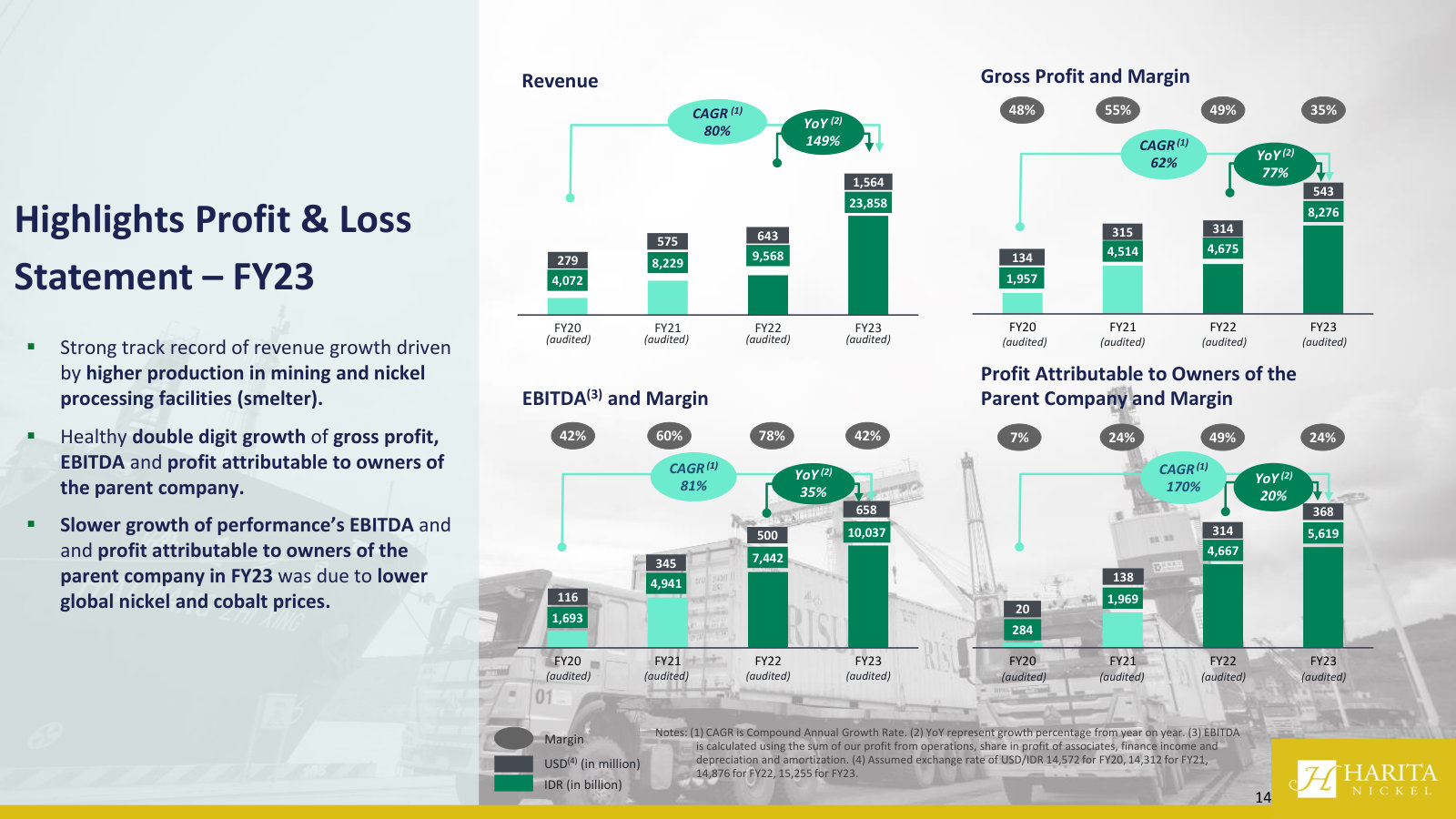

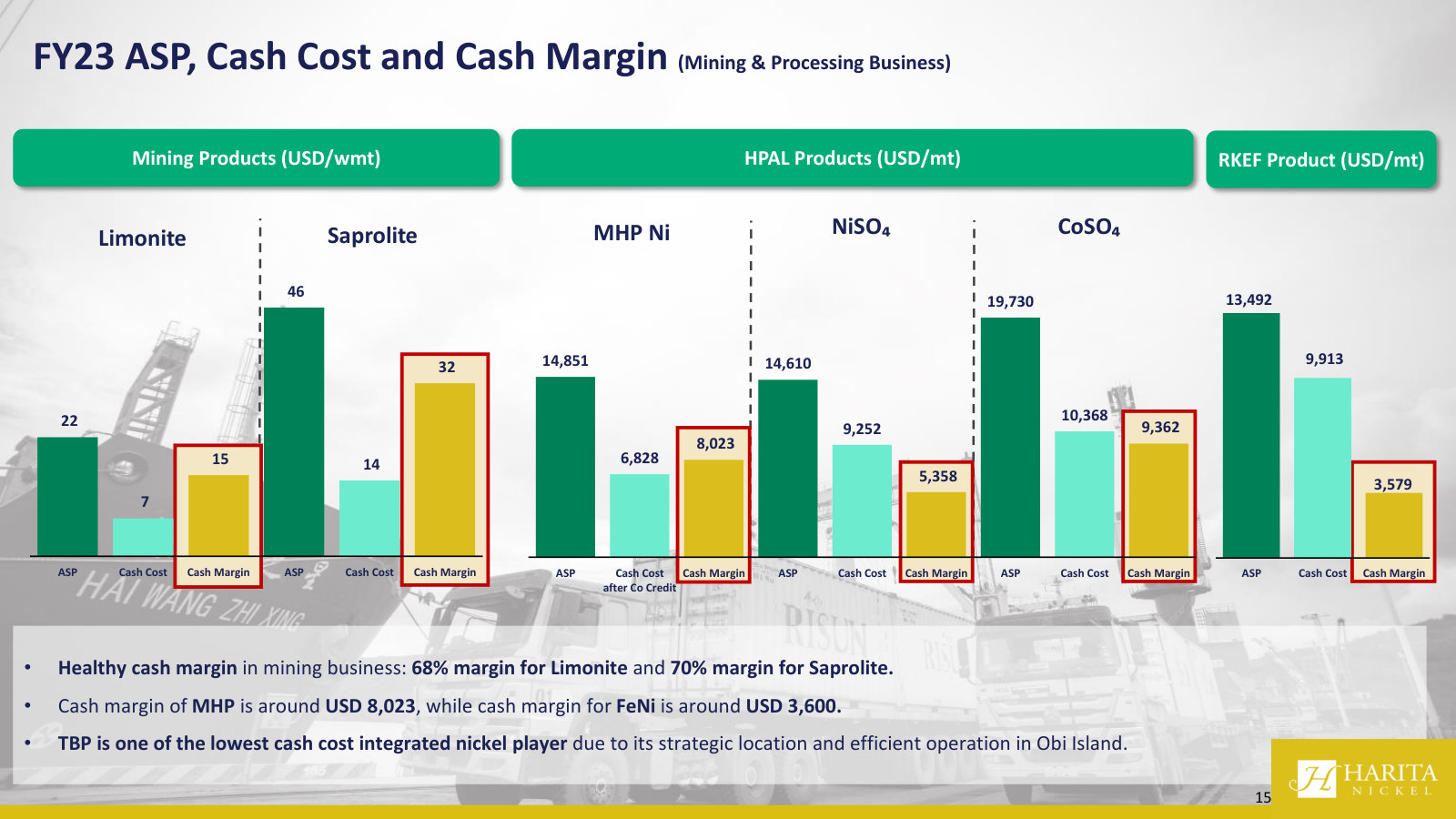

p. 4 — Journey in 2023: the April 2023 IPO and the ramp-up of RKEF and HPAL lines producing MHP, nickel sulfate, cobalt sulfate and ferronickel. · Open the full presentation →p. 5 — Mining operations: limonite and saprolite ore output feeding the smelters, from two operating mines with three more in exploration. · Open the full presentation →p. 6 — Obi Island map: mines, HPAL/RKEF smelters, ports and captive power all co-located — the short-haul integration behind the low-cost claim. · Open the full presentation →p. 7 — HPAL route: MHP, nickel sulfate and cobalt sulfate output — the battery-grade chemicals side of the business. · Open the full presentation →p. 9 — RKEF route: ferronickel (FeNi) output for stainless steel — the second, longer-established processing line. · Open the full presentation →p. 11 — Ports at Obi Island: the captive jetties that bring coal in and ship MHP, nickel sulfate and FeNi out. · Open the full presentation →p. 12 — Capacity growth plans by product: defines MHP vs FeNi and lays out the path from 62kt to a planned 425kt of contained Ni/yr. · Open the full presentation →p. 14 — P&L highlights FY20–FY23: revenue, gross profit, EBITDA and profit to owners with margins — the scale-up and where margins sit. · Open the full presentation →p. 15 — ASP, cash cost and cash margin by product — limonite, saprolite, MHP, nickel/cobalt sulfate, FeNi: how each line actually earns. · Open the full presentation →

Analyst Call 9M25 — 9M25 · 22 pages · The last analyst-call deck before the Public Expose — 9M25 financials and construction progress on KPS, quicklime and iron extraction. · Open →

Company Presentation FY24 (Analyst Call) — FY24 · 20 pages · The FY24 full-year numbers and the project pipeline (KPS, GTS mining, quicklime, jetties) as management framed it a year earlier. · Open →

Company Presentation 9M24 — 9M24 · 23 pages · Carries the 2024 ore reserves table and the launch of electrolytic cobalt — reserve base and product detail absent from the featured decks. · Open →

Company Presentation 9M23 — 9M23 · 30 pages · The first post-IPO deck: reserve base, reserve-replacement strategy, and the GTS/KTS/GPS acquisitions that expanded the resource. · Open →